Glittering and glamorous, with a lifestyle to match the best in the world, the “little red dot” named Singapore has an aspirational quality to it — it has one of the highest per capita GDP numbers; one of the best-integrated multi-racial societies; and thanks to the superhit movie Crazy Rich Asians, the island’s reputation as a wealthy nation is gilt-edged.

To put things in perspective, though Singapore has a population of just over 6 million, World Bank data for 2023 show that its per capita GDP (USD 84,734.3) is 73 per cent more than the global average of high-income countries (USD 48,752.7). Under this metric, Singapore’s next-door neighbour Malaysia has USD 11,379.1 and Asian giant China has USD 12,614.1.

In terms of per capita GDP, Singapore outranks even the United States of America (USD 82,769.4) and is far ahead of economies like Australia, Japan, Germany, United Kingdom, United Arab Emirates, and India.

In this context, how much money would a person in Singapore need to retire and spend their days in comfort? The very high per capita GDP figure may give the impression of everyone living a lavish life in Singapore, but the reality is more complicated than that.

Speaking to Connected to India about retirement planning, a Singapore-based Indian-origin investment specialist says that a moderately comfortable post-retirement life in Singapore — with a domestic help, cable and Internet, occasional small indulgences, some taxi rides, airfare for an annual round trip to India — would cost about SGD 100,000 (USD 77,300 approx) a year. This does not even cover any luxuries like frequent dining out or exotic vacations.

The figure of SGD 100,000 a year is based on the assumption that the retiree has no outstanding loans, including a house loan, and has bought adequate health insurance.

Schooling is one of the major expenses for parents in Singapore — this is not an expense they can or want to compromise on. Sending a child to junior school costs SGD 25,000 and to senior school costs SGD 50,000, “and that’s just the fees, not counting the extras”, says the finance expert. These fees are for international schools in Singapore. “Local schools are subsidised and close to free; but have a priority order for enrolment — citizens first, then permanent residents, and then employment pass holder families. The quality of education in local schools is high,” he adds.

A couple with two children needs SGD 100,000 a year just to put their kids through international school. Over a decade, that adds up to a million Sing dollars just for school fees. Such expenses can hit the retirement fund, but people must try harder and practise financial discipline.

As one advances in years, spending on health care tends to rise; it does so for most people. The investment specialist tells us, “Health care in Singapore is not as expensive as in the United States, but I would say it’s probably 50 per cent of that — as a guesstimate. So, if it costs SGD 60,000 (USD 47,092 approx) in America for a certain type of surgery, it might cost SGD 30,000 (USD 23,546 approx) in Singapore. To give you a comparable figure for India, that [same surgery] would cost something like INR 5 lakh (SGD 7,400 approx or USD 5,800 approx). This cost, of course, would be for expensive treatments and surgeries in Singapore, not for regular consultations.”

Treatment at Singapore government hospitals is subsidised, but “a part of that comes from your savings”. So, add some health care costs, too, to your post-retirement expense sheet.

That brings us to the longevity of the average Singaporean and the retirement age. Average life expectancy in Singapore now is 83 years (80.7 years for men and 85.2 years for women), a good decade longer than the global average of 73 years. Factoring this in, and aligned with the global trend in advanced economies, Singapore has been raising its retirement age.

The Singapore Ministry of Manpower informs: “In accordance with the Retirement and Re-employment Act (RRA), from 1 July 2022, the minimum retirement age is 63 years. Your company cannot ask you to retire before that age.”

It adds: “The retirement age will be raised to 64 years from 1 July 2026. It will be applicable to those born on or after 1 July 1963.”

As per available information, the retirement age in Singapore is likely to be raised to 65 by the year 2030.

Raising the age ceiling for retirement is not always welcomed by the workforce — France, for example, saw widespread protests by trade unions in January 2023 over a proposal to increase the retirement age from 62 to 64 — but a delayed retirement does give one the opportunity to save more and prepare better for living on a smaller income.

In Singapore, the “minimum age” of retirement is designed to be a protection, and it is meant for Singapore citizens and Singapore permanent residents, who have joined their employer before they turned 55.

This protection is essential, at least for those who are able to keep working. The investment specialist says, “Singapore is not cheap if you don’t have an income. The house, even if it’s fully paid for, needs maintenance, on top of other regular expenses. That’s why you’ll see many older people still working in Singapore.”

He also points out, however, that raising the retirement age “is a mechanism of signalling by the government but it’s not binding on anyone outside the government”.

Private sector workers in Singapore, therefore, like private sector workers anywhere in the world, have to prepare themselves for retiring sooner than public sector employees, and work harder to save up. This preparation includes looking at the inflation trend in Singapore and calculating how much, say, 100 Singapore dollars can buy after five years, compared to what it buys now.

The nominal inflation rate in Singapore — the simple graph of rising prices without taking into account any change in purchasing power — is not very high, he points out, pegging it at 2.5 per cent to 3 per cent. But there is a flat rate of 9 per cent Goods and Services Tax on everything, and any GST increase also means an overall price increase. A retiree needs to budget for those price hikes, too.

Incidentally, Singapore Prime Minister and Finance Minister Lawrence Wong had said (when he was deputy PM) at the end of February 2024 — during the debate on the Singapore Budget statement — that there would be no need for any further GST hikes until the end of this decade. “We have closed the funding gap up to 2030. The GST increase that we announced was intended for this, so we are okay up to 2030. We do not need further GST increases up to 2030,” he said.

Even with no further GST hikes, some retirees in Singapore will undoubtedly struggle to pay the bills. The Singapore Government helps out by giving cost-of-living financial assistance to eligible beneficiaries, but relying on that to live a comfortable retired life is not smart planning.

How to make a nice, full retirement pot in Singapore

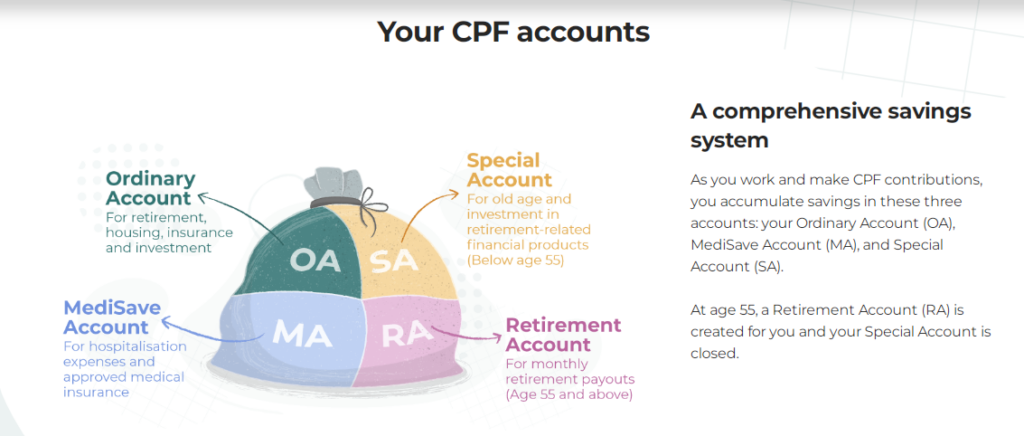

The savings instruments available are not very different for a Singapore citizen and a permanent resident, since the Central Provident Fund is applicable to both.

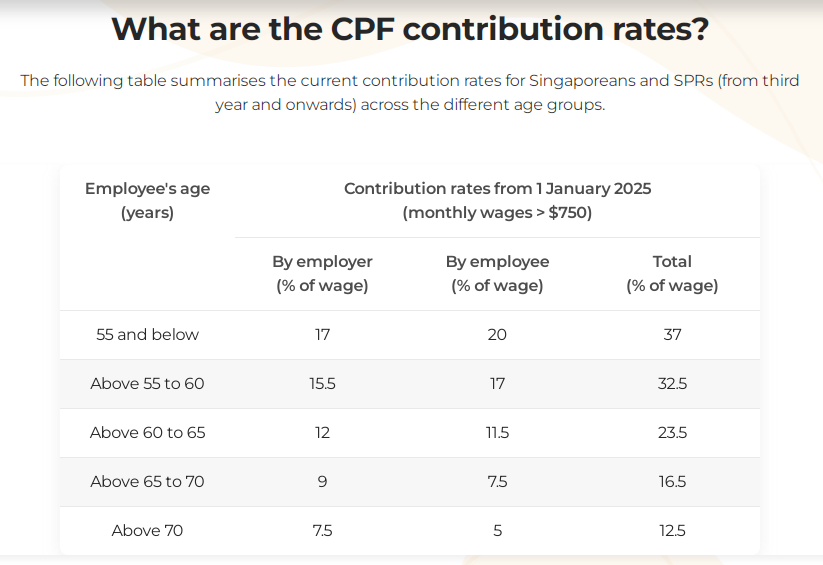

Anyone with a salary in Singapore has to compulsorily put 20 per cent of that, up to a sum of SGD 1,480, into the CPF, and then the employer puts in a corresponding percentage (17 per cent) of one’s wages. This money goes into different types of CPF accounts and keeps growing with the interest accrued.

Point to note, says the investment specialist: “Anyone with a salary has to mandatorily contribute 20 per cent, but the contribution cap, as of now, is SGD 1,480. When your salary is SGD 1,000, then your CPF contribution is SGD 200. When your salary is SGD 5,000, then your CPF contribution is SGD 1,000. When your salary is SGD 7,400, then your CPF contribution is SGD 1,480. But after that, even if your salary is a million dollars, your mandatory CPF contribution is still SGD 1,480 — the limit has been reached. There are plans to increase the salary ceiling to SGD 8,000 in 2026, thereby taking the upper limit of the CPF contribution to SGD 1,600.”

Another point to note: “A salaried employee in Singapore can voluntarily add more money into the CPF account, even after reaching the current SGD 1,480 limit, but the CPF treatment given to the additional amount is different. The rate of interest earned by this additional contribution will be lower than the rate of 4 per cent interest earned by the mandatory CPF contribution.”

“The mandatory contribution into CPF goes into several different buckets. A saver can use the CPF fund in the general bucket to make a down payment for a house, but cannot touch the fund in the medical bucket,” says the specialist.

He points out that the down payment for a property is “significantly large”. For instance, if one buys a million dollar property, one has to put up SGD 200,000 (USD 155,000) as down payment. Therefore, savings beyond CPF are also necessary to meet this goal. “Moreover, when you take money out of the CPF housing bucket to purchase a property, try to replenish that CPF amount later on, if you can; then your money keeps growing,” he says.

The investment specialist gives us some pointers to create a retirement pot that is substantial enough to acquire a property and live in at least basic comfort in Singapore.

● No matter what your income, take a little bit out of it every month, and create the discipline of saving. Start this as early as possible in life; teach your children to do the same. As your income goes up, increase that “little bit” instead of spending freely on discretionary lifestyle items.

● Divide your savings into pieces. The biggest piece goes towards buying a house or saving up for it. Make this piece as big as you can, even when you must stretch your money.

● Save for the long haul. Do not touch your savings for anything other than a life-threatening situation. Do not even look at it and stress about the return on investment. Just keep putting the money in, and never take it out until it is time to meet the goal for which you were saving, e.g. a property purchase or children’s education.

● Singapore citizens are helped by the Singapore Government to acquire an HDB property. Eligible people should absolutely invest in that. Singapore permanent resident (SPR) households can also own HDB property, but that comes with certain limitations.

● Get medical insurance even when you are young and do not feel the need for it. The younger you are, the lower the premium. Increase the medical insurance coverage as your family grows. Again, stretch for it, and get as much coverage as possible within your income. This ensures you do not have to take money out of your retirement fund to meet sudden medical expenses.

● Gather knowledge about investment avenues and identify your risk appetite, i.e. the capital you are prepared to lose if the investment goes bad. Rule of thumb: the higher the returns, the higher the risk; the lower the returns, the lower the risk. Do not invest a large amount in an investment instrument you do not fully understand. Do not get persuaded to invest without enough information. It takes time to learn these things.

● Equity (stocks) is risky but can fetch higher returns than debt (fixed deposits) instruments, and investing in equity is preferable when you are young — without too much capital to lose and with enough working years ahead of you to recoup any losses — but learn and seek advice and do not be heedless.

● Think about your life and imagine where you want to be when you retire. For an Indian-origin permanent resident in Singapore, whose children are growing up in the island nation, the saved up Singapore dollars might buy a lot more luxury back home in India, but would you rather go back to India or stay in Singapore?

● In your zeal to save, do not forget to live. See the world when you can, and do not keep it all for your golden years. It is important to get that exposure for personal growth and even professional advancement.

How to calculate your post-retirement monetary needs

“The inflation figures in Singapore are not that high — usually about 3 per cent — and the CPF gives you interest of 4 per cent in your Retirement Account, so your retirement savings grow,” says the investment specialist.

As to how much a Singapore citizen or permanent resident might need 30 years down the line, he estimates, “the current requirement of SGD 100,000 a year — to live a comfortable retired life in Singapore — will become SGD 150,000 after 10 years, and then SGD 200,000 after 20 years, and then SGD 250,000 after 30 years, and so on. Basically, your living expenses are likely to increase by SGD 50,000 every 10 years, all other factors remaining the same”.

A young Singapore employee or a self-employed person ought to start saving for this long-term horizon — and start as early as possible — and not just for short-term goals.

Taking your cue from the CPF model of savings being put into different buckets, each with a specific purpose, create your own designated retirement fund and recreation fund, and do not touch the retirement pot, unless it is life and death.

“It’s a very costly mistake if you don’t do it at an early age. It is very, very important to do it, because there are no second chances on this,” says the investment specialist. “When you start worrying about it, you can only worry because there’s nothing you can do about it. People often don’t do what they should when there’s still time to do something about it. So, starting early to save for retirement is very important.”