The bond market in India is quite vibrant, particularly for sovereign bonds. And, in order to be an informed investor either in the market directly or through the mutual fund route, one must have clarity on some of the basic structure and terminology of the Indian market.

It is also important to understand that sovereign bonds are basically market borrowings that the government undertakes to bridge the fiscal deficit, i.e. a part of the government debt arising from the excess of government spending over revenues. Further, since India has a Union Government or a Central Government as well as state governments, there is a Union Budget and a State-wise Budget that addresses the needs of the respective governments and therefore also addresses the extent of borrowing that is necessary for the Union and State Governments.

The sovereign bonds market or the risk-free bonds market in India has essentially three segments:

Government Securities, also known as G-Secs or GOI (Government of India) bonds – these are issued by the Government of India;

Treasury Bills or T-Bills – also issued by the Government of India, and

State Development Loans or SDLs – issued by various State Governments.

G-Secs can be issued for tenures of 2 to 30 years, though the secondary market trading is more popular for tenures of 3, 5 and 10 years. Some long-term investors such as life insurance companies and pension/ retirement funds prefer to buy 15 to 30 years as and when the yields are attractive.

T-Bills are typically short-term securities, and are issued with maturities of 91, 182 and 364 days. These securities are also traded well in the market, though between institutional investors.

SDLs are similar to G-Secs in terms of issuance, though the issue and demand is historically observed for maturities of up to 10 years.

G-Secs and SDLs are usually issued with interest payable semi-annually/half-yearly, and the interest payment dates are also called coupon dates. The interest rate is also referred to as the coupon rate. The G-Secs issued for a single maturity date is generally termed as “plain vanilla” bond and is the most popular both in terms of issuance and investor demand.

However, at times variations such as floating rate bonds, zero coupon bonds, inflation-indexed bonds have seen the light of day. T-Bills are issued in the form of discounted instruments, and on maturity one receives the “face value” of the T-Bill. This means that if a T-Bill of face value of Rs 100 is bought at Rs97, on the maturity date the investor receives Rs 100 that would imply earning interest of Rs 3 for the holding period.

The central bank of the country, i.e. the Reserve Bank of India (RBI) acts like a banker to the Central and State governments and is responsible for the timing and quantum of the issue of the above three categories of securities. The RBI is also responsible for the timely servicing of the debt in terms of the interest payments and the repayment of the principal amount of the securities.

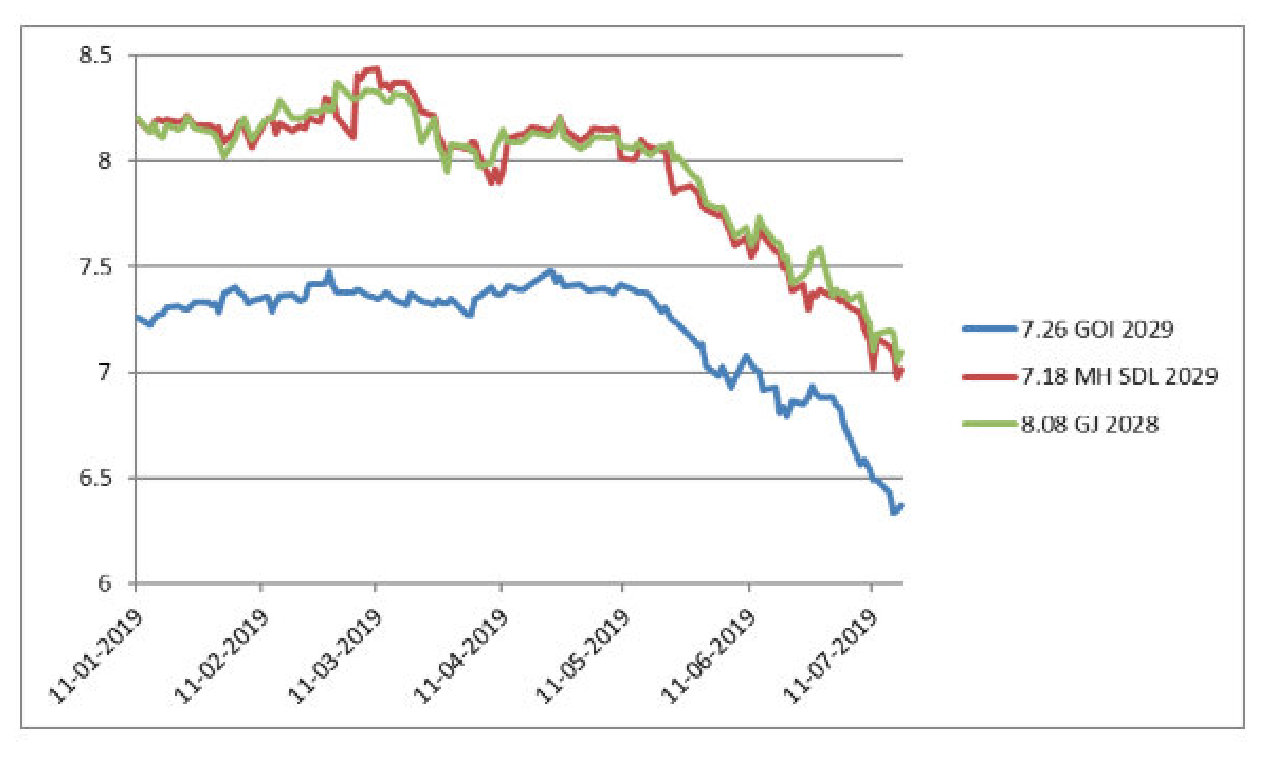

Though the issuers of the securities may differ, due to the federal structure of India and due to the RBI being empowered to service the debt, both G-Secs and SDLs are very similar in providing credit comfort to a risk-averse investor. However, technically the G-Secs and T-Bills are the sovereign securities and are deemed to be risk-free instruments from the credit point of view. And due to this technicality, it is possible to get some yield pick-up (higher returns) on SDLs over G-Secs (usually between 0.50-0.80% depending on market conditions).

Yield movement & spread of SDLs (Maharashtra & Gujarat) over benchmark 10-year G-Sec (GOI)

There is scope to participate both in the primary and secondary market for G-Secs and SDLs by individual investors, including NRIs, though the market as of now is dominated by institutional investors. G-Secs and SDLs should be considered for (credit) risk-free investments both for long-term holding as well as for trading opportunities due to the significantly higher liquidity as compared to corporate bonds.

Apart from credit risk, market risk is a different perspective and is a function of interest rates. Investing predictable medium to long-term surplus funds and holding securities till maturity could be a strategy to mitigate market risk. And to mitigate reinvestment risk, rebalancing the portfolio by selling securities once they become short term and buying new securities of longer tenor could be considered. Rebalancing, however, involves transaction and other costs and would need to be executed with professional help.

Tweet us on @connected2india or email us on info@connectedtoindia.com for your specific queries and subjects you would like us to write on.

Note: Connected to India articles on NRI personal finance are intended to help Non-Resident Indians (NRIs) understand the increasingly complex world of financial investments. It is not a solicitation, recommendation, endorsement, of any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.