A large investor who read my last article on Indian bonds in this website remarked that “debt is the new equity”, implying that the debt market (aka the bond market) is now being preferred over the stock (equity) market by investors for attractive and sustained returns.

Indian stock market indices (NSE Nifty and BSE Sensex) are near all-time highs and economic growth has declined significantly, and thus going forward the expectations are low for high returns in the stock market. And as economic growth needs a boost for revival, interest rates have started coming down. As rates go down so do yields, and as yields go down bonds are in profit.

An NRI planning to invest in the Indian bonds market can do so through the portfolio investment scheme (PIS) offered by the Reserve Bank of India (RBI). Your banker (India-based) or your investment advisor will easily take care of this, including opening a “demat” account that will house all your investments (both stocks and bonds). The investments however must be carried out in accordance with the regulations and can be done with your PAN card. If you are overseas at the time of opening the NRI demat account, all the copies of the documents need to be attested by the Indian embassy. If you are in India, carry the originals, the bank staff will attest the copies.

An NRI can buy bonds on repatriable basis using funds in the Non-Resident External (NRE) account and on non-repatriable basis with an NRO account. An NRI will have to first close her/his existing demat account, if she/he had opened one before acquiring NRI status. The stocks or bonds in the existing demat account, if any, would need to be transferred to an NRO (Non-Resident Ordinary) demat account. It is important to note that the NRI demat account cannot be opened or operated by an Indian Power-of-Attorney holder.

The interest on the bonds is not taxable in India and is repatriable if the investment is made from the NRE account or from an FCNR account. However, if there is a trading opportunity to be availed of, capital gains arising from short term or long term investments would be liable to tax in India and withholding tax or tax deduction at source (TDS) would be at 20% of the gains. If an NRI has income only from these investments and TDS has been deducted, there would be no necessity to file an income tax return. However, it is best to consult your tax consultant and investment advisor before you commence your investment activities.

An alternate way to invest in Indian bonds and that too without much of regulatory compliance and frequent portfolio monitoring, is to use the mutual fund route. The investment amount can be directly debited from NRE or NRO accounts. On redemption (exit from the fund), the amount shall be directly credited to the investor’s account. And, as in the case of direct bond investments, for debt mutual funds too, NRIs would be subject to withholding tax/ TDS on the capital gains.

However, quite a few of the Indian mutual fund houses do not accept investments from NRIs based in the USA or Canada. This is due to the complex compliance requirements under Foreign Account Tax Compliance Act (FATCA). This all involves a lot of paperwork and compliance on the part of mutual fund houses. So, certain mutual fund houses have stopped accepting investments from NRIs based in the US and Canada. Subject to confirmation from the mutual fund houses, investment may be made in the various bond funds of Axis, Aditya Birla Sunlife, DSP, Edelweiss, HDFC, ICICI Prudential, Kotak, Reliance, SBI, Tata, to name a few.

NRIs from Singapore, Middle East, UK, Europe have no such restrictions, though certain simple declarations or documentation may need to be provided to the fund house.

For only mutual fund investments, no demat account is necessary. For the investments and redemptions made, the mutual fund sends a statement directly to the investor. As per the regulatory (SEBI) guidelines, a consolidated account statement (CAS) details all the transactions and investor’s holding at the end of the month across all schemes of all mutual funds, by an investor. A CAS for each calendar month is issued to the investors in whose folio transactions have taken place during that month. A CAS every half yearly (September/ March) is issued, detailing holding at the end of the six-month period, across all schemes of all mutual funds, to all such investors in whose folio no transaction has taken place during that period.

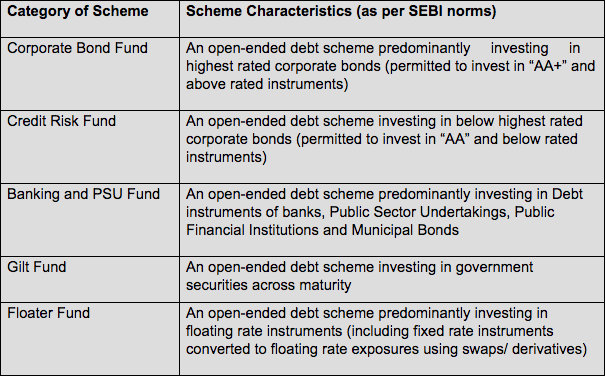

Debt Mutual Funds to be considered for investment:

Tweet us on @connected2india or email us on info@connectedtoindia.com for your specific queries and subjects you would like us to write on.

Note: Connected to India articles on NRI personal finance are intended to help Non-Resident Indians (NRIs) understand the increasingly complex world of financial investments. It is not a solicitation, recommendation, endorsement, of any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.